Is It Hard to Get USDA Approved?

For many homebuyers, that’s the first question that comes up before applying for a USDA loan. The short answer is: not necessarily. In fact, USDA loans are often easier to qualify for than conventional mortgages because they offer flexible credit guidelines, no down payment requirements, and lower upfront costs. But approval still depends on several important factors, including your income, credit score, debt levels, employment history, and whether the property is located in a USDA-eligible rural area.

This is where many applicants get confused. Some buyers assume USDA loans are guaranteed because they are government-backed. Others believe the process is too difficult or takes too long. The reality is somewhere in between. USDA loans are very achievable for qualified borrowers, but the approval process is detail-driven and requires proper preparation. Even small issues like incomplete paperwork, high debt-to-income ratios, or choosing an ineligible property can delay approval or lead to denial.

Understanding the full usda loan approval process before applying can significantly improve your chances of success

USDA Loan Approval Process (Step-by-Step)

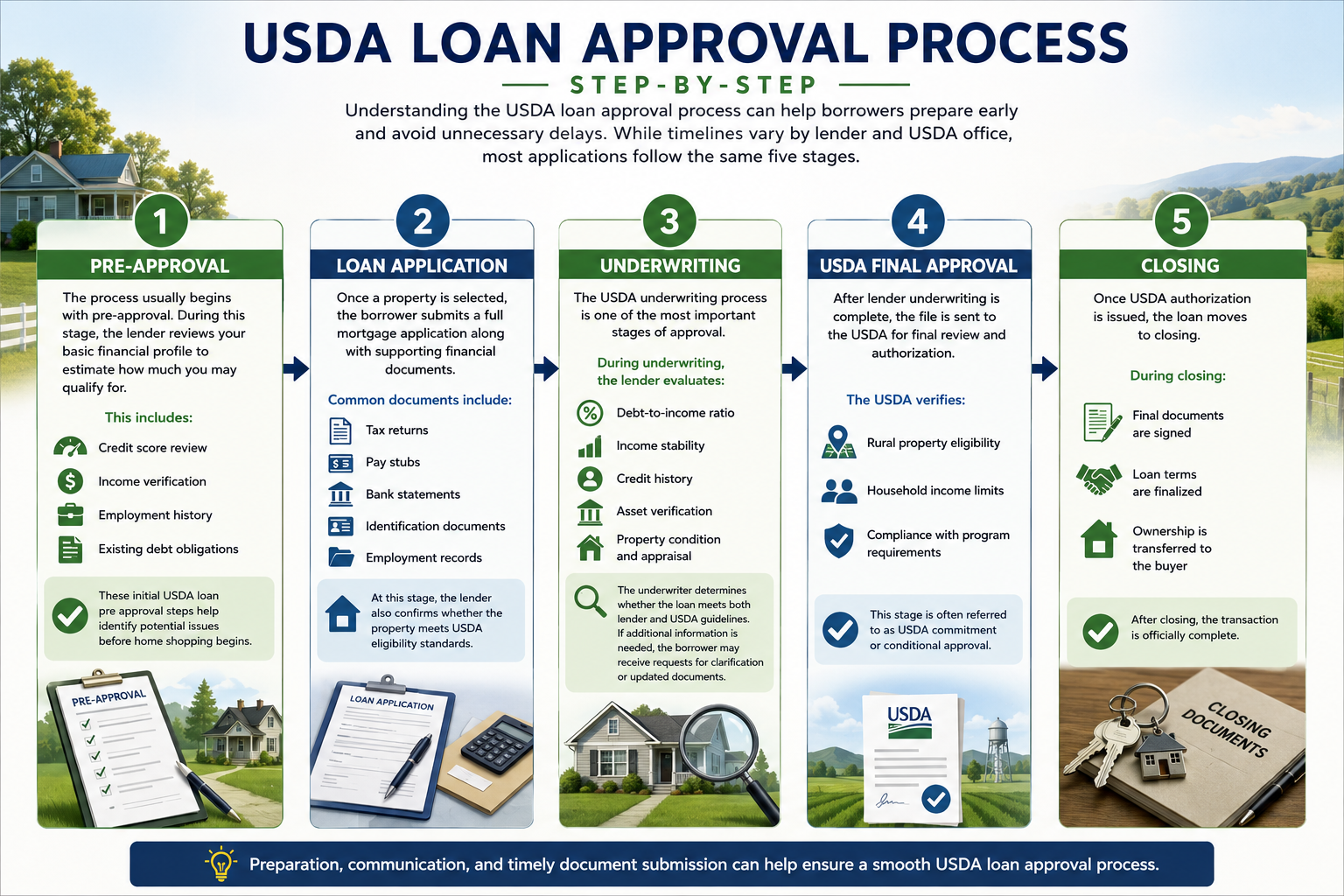

Understanding the usda loan approval process can help borrowers prepare early and avoid unnecessary delays. While timelines vary by lender and USDA office, most applications follow the same five stages.

1. Pre-Approval: The process usually begins with pre-approval. During this stage, the lender reviews your basic financial profile to estimate how much you may qualify for.

This includes:

- Credit score review

- Income verification

- Employment history

- Existing debt obligations

These initial usda loan pre approval steps help identify potential issues before home shopping begins

2. Loan Application: Once a property is selected, the borrower submits a full mortgage application along with supporting financial documents.

Common documents include:

- Tax returns

- Pay stubs

- Bank statements

- Identification documents

- Employment records

At this stage, the lender also confirms whether the property meets USDA eligibility standards.

3. Underwriting: The USDA Underwriting process is one of the most important stages of approval

During underwriting, the lender evaluates:

- Debt-to-income ratio

- Income stability

- Credit history

- Asset verification

- Property condition and appraisal

The underwriter determines whether the loan meets both lender and USDA guidelines. If additional information is needed, the borrower may receive requests for clarification or updated documents.

4. USDA Final Approval: After lender underwriting is complete, the file is sent to the USDA for final review and authorization.

The USDA verifies:

- Rural property eligibility

- Household income limits

- Compliance with program requirements

This stage is often referred to as USDA commitment or conditional approval.

5. Closing: Once USDA authorization is issued, the loan moves to closing.

During closing:

- Final documents are signed

- Loan terms are finalized

- Ownership is transferred to the buyer

After closing, the transaction is officially complete.

How Long Does USDA Loan Approval Take?

One of the most common questions borrowers ask is: usda loan how long does it take?

In most cases, the full usda loan approval time ranges between 30 and 60 days. However, timelines can vary depending on the lender, USDA processing volume, and how quickly documents are submitted

- Pre-approval: 1–3 days.

- Underwriting: 1–2 weeks.

- USDA Review: 1–3 weeks (this varies by state office backlog).

- Closing: 1 week.

The biggest delays usually come from missing documentation or a slow appraisal. Getting your papers in order before you even find a home can shave weeks off this timeline.

How Long Does USDA Approval Last?

Once approved, USDA loan approval is generally valid until closing, although lenders may require updated financial documents if delays occur.

How Long Is USDA Pre-Approval Valid?

Most USDA pre-approvals remain valid for approximately 60 to 90 days. If the home search takes longer, lenders may request updated income or credit information.

USDA Loan Approval Requirements

Understanding usda loan approval requirements early can help borrowers avoid delays and improve approval chances.

While guidelines vary slightly by lender, most USDA loans evaluate four major areas.

1. Credit Score Requirements: The standard benchmark for usda loan credit score requirements is typically 640 or higher.

- 640+ usually qualifies for automated underwriting

- Below 640 may require manual underwriting and additional review

A higher score can improve approval chances and reduce processing delays. Lenders also review your payment history, collections or bankruptcies, credit utilization & overall financial behavior.

2. USDA Loan Income Limits: USDA loans are designed for low- to moderate-income households. USDA loan income limits vary based on:

- Location

- Household size

- Local median income levels

Importantly, USDA considers total household income, not just the borrower’s salary. Applicants whose income exceeds local USDA limits may not qualify, even with strong credit.

3. Debt-to-Income Ratio: The usda loan debt to income ratio helps lenders determine whether the borrower can comfortably manage monthly payments. Typical USDA guidelines recommend:

- 29% maximum housing ratio

- 41% total debt-to-income ratio

Some borrowers with strong credit or additional savings may still qualify with slightly higher ratios. Reducing debt before applying can significantly improve approval odds.

4. Property Requirements: The property itself must meet specific usda loan property requirements. The home must:

- Be located in usda eligible rural areas

- Serve as the borrower’s primary residence

- Meet basic safety and livability standards

Properties with major structural issues, investment properties, or vacation homes generally do not qualify under USDA guidelines because location eligibility is critical, many borrowers verify property eligibility before making an offer

What Disqualifies You from a USDA Loan?

Many borrowers meet the basic requirements for a USDA loan but still face rejection during the approval process. Understanding the most common reasons for usda loan denial can help applicants avoid mistakes before applying.

One of the biggest reasons for denial is income eligibility. USDA loans are designed for low- to moderate-income households, so applicants whose income exceeds local USDA limits may not qualify, even if they have strong credit and stable employment.

Poor credit history can also create problems during underwriting. Late payments, collections, recent bankruptcies, or high credit utilization may raise concerns for lenders reviewing the application.

Debt levels are another important factor. If a borrower has too much monthly debt compared to income, the lender may determine that the loan payment is not affordable. This is especially true when the debt-to-income ratio exceeds USDA guidelines.

Property eligibility is another common issue. USDA financing only applies to homes located in eligible rural areas, and the property must meet minimum condition standards. Investment properties, vacation homes, or homes needing major repairs are often denied.

Employment stability also matters. Lenders prefer borrowers with consistent and verifiable income. Frequent job changes, gaps in employment, or irregular income may increase underwriting risk.

Many buyers ask: Why would you be denied a USDA loan?

In most cases, denial happens because of one or more of the following:

- Income exceeding USDA limits

- Low credit score or poor repayment history

- High debt-to-income ratio

- Ineligible property location or condition

- Incomplete documentation

- Unstable employment or inconsistent income

The good news is that many of these issues can be corrected before applying.

USDA Loan Approval Rate – How Likely Are You to Get Approved?

There is no universal usda loan approval rate, because approval depends heavily on the borrower’s financial profile and the property being purchased.

Unlike conventional loans, USDA loans focus strongly on overall affordability and eligibility rather than just credit score alone. This means approval is often more achievable for borrowers with moderate income and stable financial habits.

Several factors affect approval likelihood, including:

- Credit history and score

- Household income

- Debt-to-income ratio

- Employment consistency

- Property eligibility

- Accuracy of submitted documents

One of the most overlooked factors is documentation. Even financially qualified borrowers can experience delays or denials because of missing paperwork or incomplete financial records. The approval process is also more predictable when borrowers prepare early. Applicants who understand USDA requirements, reduce debt, and organize documents before applying are usually in a much stronger position rather than thinking about approval as luck, it is more accurate to view it as preparation-driven. In many cases, usda loan approval is highly controllable when borrowers meet the guidelines and avoid common application mistakes.

What Is the Minimum Credit Score for USDA Loan Approval?

Technically, the USDA doesn’t set a hard minimum. However, most lenders require a 640 score for usda loan credit score requirements. If your score is below 640, you may still be approved through “manual underwriting.” This involves an underwriter personally reviewing your financial life to see if you have “compensating factors,” like a large amount of savings or a long history of on-time rent payments.

Manual Underwriting Possibility

Borrowers with lower scores may still qualify through manual underwriting if they show strong compensating factors such as:

- Stable income

- Low debt levels

- Savings reserves

- Strong rental payment history

Manual underwriting usually requires more documentation and takes longer than automated approval.

Tips to Improve Your Credit Score Before Applying

Borrowers can improve approval chances by strengthening their credit profile before submitting an application. Helpful steps include:

- Paying bills on time consistently

- Reducing credit card balances

- Avoiding new debt before applying

- Correcting errors on credit reports

- Keeping older credit accounts open

Even small credit improvements can make a meaningful difference during the USDA approval process.

What disqualifies a property from USDA financing?

The property itself must meet usda loan property requirements. You can check your potential home’s eligibility on the official USDA map.

Properties are disqualified if they are:

- Located in an urban area (typically towns over 35,000 people).

- Income-producing (like a working farm or commercial storefront).

- In poor structural condition (leaking roofs, broken HVAC, or safety hazards).

USDA vs FHA loan – which is better?

For most rural buyers, usda guaranteed loan vs direct loan comparisons show that USDA wins on cost. FHA requires a 3.5% down payment and higher monthly mortgage insurance. USDA requires 0% down and has a lower annual fee (0.35%). If your home is in an eligible area, USDA is almost always the more affordable choice.

How to increase your chances of USDA loan approval

If you want to how to improve loan approval chances, follow these actionable steps:

- Lower your DTI ratio: Pay down a credit card or car loan before applying. Even a $50/month reduction in debt can make a difference.

- Maintain stable employment: Avoid switching jobs or moving from a salary to a commission-based role right before you apply.

- Gather 3 months of reserves: Having enough cash in the bank to cover three months of mortgage payments is a powerful “compensating factor” that underwriters love to see.

- Submit a complete file: Missing just one bank statement can pause your application for days. Use a checklist to ensure every page of every document is included.

Comparison visual between USDA Guaranteed vs. Direct Loans

Documents required for USDA loan approval. To keep your usda loan pre approval steps moving, have these ready:

- Income proof: Last 2 years of W-2s and federal tax returns.

- Pay stubs: Your most recent 30 days of pay.

- Asset statements: Last 2 months of bank statements for all accounts.

- Identity: Government-issued ID and Social Security card.

- Explanations: Be ready to write a brief letter for any large deposits or credit inquiries.

USDA guaranteed vs direct loan – approval differences

It’s important to know which program you are applying for. The usda guaranteed loan vs direct loan difference matters for approval:

- Guaranteed Loans: Handled by private lenders. Best for moderate-income households. These are generally faster to close.

- Direct Loans: Handled directly by the USDA. Best for low and very-low-income families. These often have lower interest rates (as low as 1% with subsidies) but can take longer due to government backlogs.

Try August Brown for technology-focused advisory

August Brown is a boutique technology-focused management consulting and advisory firm specializing in feasibility studies. We provide deep insights and analytical rigor that drive growth strategies and market positioning for organizations across the public and private sectors. If you are looking for expert due diligence or commercialization strategies for new technologies, our team intimately works with you to accelerate growth and solve complex adoption issues.